By liquidating (Chapter 7) or restructuring (Chapter 13) debt, bankruptcy gives overburdened customers a chance to make a fresh start. The bankruptcy court is called “acquittal” of debts in both situations. This means that debtors lose their right to take legal action against them, including to try to collect a debt or recover property. Consumers […]]]>

By liquidating (Chapter 7) or restructuring (Chapter 13) debt, bankruptcy gives overburdened customers a chance to make a fresh start. The bankruptcy court is called “acquittal” of debts in both situations. This means that debtors lose their right to take legal action against them, including to try to collect a debt or recover property. Consumers […]]]>By liquidating (Chapter 7) or restructuring (Chapter 13) debt, bankruptcy gives overburdened customers a chance to make a fresh start. The bankruptcy court is called “acquittal” of debts in both situations.

This means that debtors lose their right to take legal action against them, including to try to collect a debt or recover property.

Consumers can take a break and start improving their credit scores after filing for bankruptcy. What debts can and cannot be discharged in bankruptcy is a recurring question.

Giving debtors a “fresh start” in their financial lives by relieving them of onerous obligations is one of the primary goals of federal bankruptcy legislation passed by Congress.

Although society values second chances, bankruptcy is not the only option. Some debts cannot be discharged, while others are extremely difficult.

Hiring a lawyer who can advise you on bankruptcy can help you make the best choices for your particular situation.

Two different types of personal bankruptcy

What exactly is Chapter 7?

Chapter 7 may be your best bet if you don’t have enough income to cover your credit card debt, medical bills, utility bills, payday loans, or personal loans. The procedure will be completed in a few months, allowing you to start restoring your credit quickly.

You will have little or no debt when your Chapter 7 is discharged, and creditors may believe that you will be better able to repay your loans in the future.

A few months after filing for Chapter 7 bankruptcy, many people finance cars and are approached for unsecured credit. Also, two years after receiving your discharge from bankruptcy, you may be qualified to buy a home.

To find out if Chapter 7 is right for you, it’s best to check out the best credit repair companies because you may not need bankruptcy. It is crucial to study the information and discuss the options with the lawyers.

What exactly is chapter 13?

A consumer debt restructuring plan known as Chapter 13 allows debtors to settle their commitments over three to five years with one affordable monthly payment.

The Chapter 13 bankruptcy option can help you regain control of your finances from creditors who repossess your car or seize your home.

With a court-approved repayment plan that you can afford, Chapter 13 allows you to pay off some of your debt. The remaining qualified debt is discharged after the repayment plan has been satisfactorily completed.

You will also be freed from the teasing of creditors since they have to suspend all collection efforts for the entire repayment period.

For homeowners who want to keep their assets secured but have more equity than they can protect with their Ohio bankruptcy exemptions, or those whose income is too high to qualify for Chapter 7 bankruptcy, Chapter 13 bankruptcy is sometimes the best option.

You need to have a steady source of income and a little extra cash to dedicate to your Chapter 13 payment plan to file for Chapter 13 bankruptcy.

Non-dischargeable debt in the event of bankruptcy

The purpose of Chapter 7 and Chapter 13 bankruptcy is to obtain a “discharge” from debts. If the bankruptcy court reverses these covenants, you will not be held personally liable as long as you file for bankruptcy.

Most consumer debt can be forgiven, including credit card debt and medical debt. However, some debts cannot be discharged in bankruptcy because they are not dischargeable.

These are debts that Congress has decided should not be forgiven by national policy.

Here are the 11 categories of non-dischargeable debt. In other words, even if you get your consumer debt discharged, creditors will still be able to collect on that type of debt.

Others will be released if a creditor does not dispute their ability to be released. Some non-dischargeable debts do not require a hearing.

You must provide evidence of unusual circumstances to obtain cancellation of non-dischargeable debts.

More than 1.4 million individuals filed for bankruptcy in 2011, significantly less than in 2010 (more than 1.5 million). This may mean that some Americans did not approve of the pardon, and some found an alternative.

Number of individuals and businesses that declared bankruptcy in the United States in 2010 and 2011

Source: https://www.statista.com/statistics/232502/personal-and-company-bankruptcy-rates-in-the-us/%5B/caption%5D

Source: https://www.statista.com/statistics/232502/personal-and-company-bankruptcy-rates-in-the-us/%5B/caption%5D

To continue to be non-dischargeable, other categories of non-dischargeable debt must be successfully contested by a creditor throughout the bankruptcy. At the hearing, the declarant of the bankruptcy and the creditor will have the opportunity to speak.

Nevertheless, the obligation will be terminated if the obligee does not object or if the court rejects its argument.

These debts are divided into three categories: those acquired dishonestly or under pretext; those suffered as a result of intentional and malicious damage to persons or property; and debts incurred from luxury credit card purchases totaling more than $650 that were made within 90 days of filing for bankruptcy and are owed to a single creditor.

Generally non-dischargeable debts

- Debts that were omitted from the bankruptcy petition unless the creditor was notified of the filing

- Several types of taxes

- Alimony or alimony

- Debts from a divorce or separation due to a child or an ex-spouse

- Penalties or fines due to government agencies

- Education Loans

- Debts for bodily injury caused by an impaired driving accident

- Debts associated with tax-advantaged pension plans

- Invoices from a condo or a housing cooperative

- Legal fees associated with child support or custody

- Criminal restitution, as well as other fines or legal sanctions

Alternatives to Bankruptcy for Debt Relief

Bankruptcy has adverse effects. You will have to wait ten years for the effects of a Chapter 7 bankruptcy to disappear from your credit report and seven years for those of a Chapter 13 bankruptcy.

This could make it more expensive or possibly impossible to get a credit card or borrow money in the future for things like a mortgage or car loan. It can also have an impact on the cost of your insurance.

It is important to research other debt relief alternatives before filing for bankruptcy. Negotiating with your creditors to lower your interest rates, get some of your debt forgiven, or extend the time you have to pay it off is often the first step to debt relief.

Since they will gain more from the deal than they would if you filed for bankruptcy, creditors generally benefit from the debt reduction.

Conclusion

You can use bankruptcy to get rid of debt from credit cards, medical bills, and collection calls.

Even the best-executed bankruptcy petition won’t always be enough to completely pay off your debts, including student loans and child support obligations.

A lawyer can explain the extent of the amount of debt discharged you will have.

They will describe the different types of debts and those that a Chapter 7 filing could not discharge. You will also get advice on how to manage these debts from your lawyer.

Related

Category: NEW

Credit cards are primarily a payment method, paid monthly. The importance of borrowings has diminished over the years. By Wolf Richter for WOLF STREET. Credit card balances include balances that accrue interest and balances that are paid in full by the due date such that no interest accrues. Many Americans use credit cards only as […]]]>

Credit cards are primarily a payment method, paid monthly. The importance of borrowings has diminished over the years. By Wolf Richter for WOLF STREET. Credit card balances include balances that accrue interest and balances that are paid in full by the due date such that no interest accrues. Many Americans use credit cards only as […]]]>Credit cards are primarily a payment method, paid monthly. The importance of borrowings has diminished over the years.

By Wolf Richter for WOLF STREET.

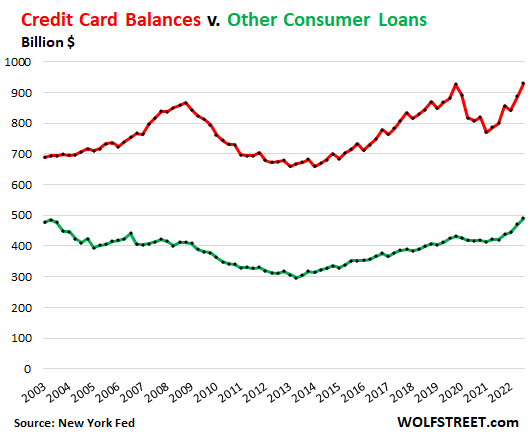

Credit card balances include balances that accrue interest and balances that are paid in full by the due date such that no interest accrues. Many Americans use credit cards only as a method of payment (and to get the 1.5% cash back or whatever), not as a method of borrowing. Thus, credit card balances are much more a measure of spending than borrowing.

Fitch estimated that the total amount paid with credit cards in the United States reached $4.6 trillion in 2021. Only a tiny fraction of the expenses were not fully repaid and added to the debt carrying interest.

In the third quarter, credit card balances rose $38 billion from the previous quarter to $930 billion, according to the New York Fed’s Household Debt and Credit Report. This $930 billion includes transactions initiated roughly in September but fully repaid in October, which do not generate interest.

Credit card spending has been boosted by the resurgence in travel, with credit cards being used as a method of payment for hotels, airline tickets, rental cars, meals, and more. Soaring costs are further increasing the amounts that pass through credit cards. But cardholders fully refunded almost all of the new amounts paid by credit card during the quarter.

Households have a lot of debt, but the problem isn’t credit cards, it’s mortgages.

In a moment, we’ll look at credit card balances as a percentage of total consumer debt and as a percentage of disposable income, and we’ll look at delinquencies and third-party collections, and we’ll see that the burden of revolving credit is not more than a small fraction of what it was in previous years and decades, and delinquencies have started to rise, but are still below pre-pandemic lows, and third-party collections have dropped to new records.

During the pandemic, plummeting reservations for airline tickets, hotels, entertainment and sports venues, restaurant meals, etc., have led to a drop in the use of credit cards as payment , and that’s where the big dip happened; it shows the collapse of expenditure on services. It is now back to normal as service spending recovers.

And yet, outstanding credit card balances in the third quarter increased by only $43 billion, showing the universal use of credit cards as a method of payment, with balances paid in full each month, and in the extent to which credit cards are used as a method of borrowing. And that makes sense because borrowing with a credit card can be ridiculously expensive, with rates as high as 30%, but paying with a credit card can earn you a kickback.

“Other” consumer loans, such as personal loans, payday loans and Buy-Now-Pay-Later (BNPL) loans, increased by $21 billion, reaching $490 billion in the third quarter . Most of them bear interest, but not all of them: for example, BNPL loans can be subsidized by the trader. These loan balances are now back to their 2003 level, despite 19 years of population growth, rising incomes and runaway inflation.

What is amazing, in fact, is how down these balances are after 20 years of population growth, income growth and inflation:

Decrease in the amount of credit card debt.

Consumers have reduced their reliance on credit card debt over the years, although credit cards have largely replaced checks and cash as payment methods. In 2021, $4.6 trillion was spent on credit cards, yet over the same period credit card balances grew by only $40 billion.

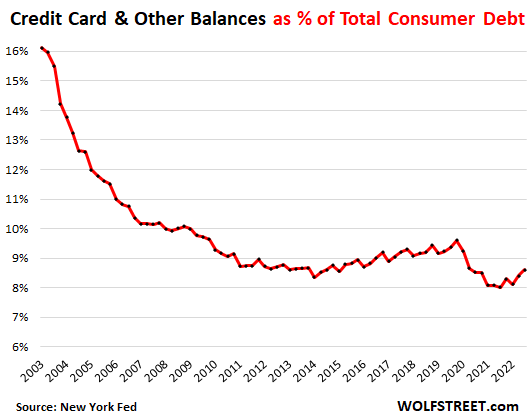

In 2003, credit card balances and other loans combined (the red and green lines in the chart above) accounted for more than 16% of total consumer debt, which also includes mortgages, auto loans and student loans. During the pandemic, this figure fell to 8%. In the third quarter, credit card balances and other consumer debt reached 8.6% of total consumer debt, roughly within the range of the pre-pandemic low in 2014.

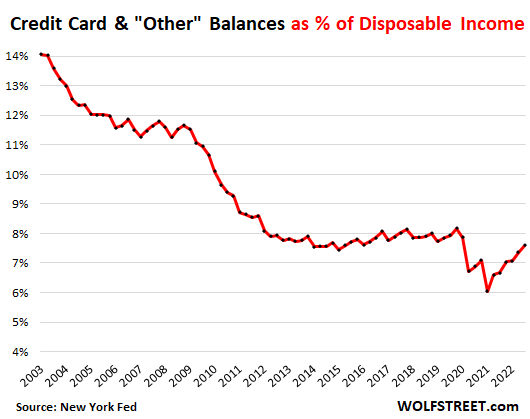

Debt burden as a percentage of disposable income.

In 2003, credit card balances and “other” consumer debt accounted for 14% of disposable income (income from all sources minus taxes and social contributions). And then over the years it fell steadily as the burden of credit card balances and “other” consumer loan balances fell relative to disposable income. In the first quarter of 2021, it fell to an all-time low of 6% as disposable income ballooned with stimulus funds. In Q3 2022, it rose to 7.6%, roughly within the range of pre-pandemic lows:

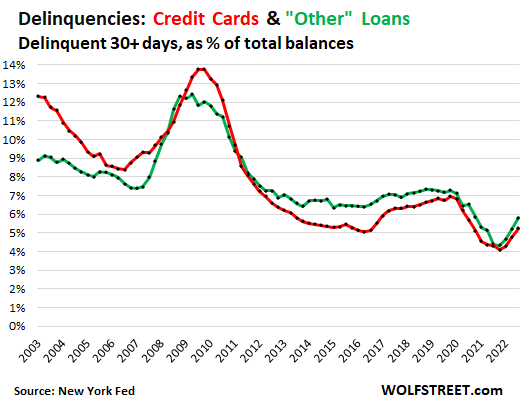

Delinquencies increase, remain at or below pre-pandemic lows.

Stimulus funds delivered directly to consumers during the pandemic – stimulus checks, PPP loans, additional unemployment benefits, etc. – as well as the sums that consumers did not have to pay – mortgage forbearance, bans on eviction, etc. dough, and many who had fallen behind on their credit cards have caught up. Others were able to enter their credit card arrears into forbearance programs, and the outstanding balance was marked “current”.

That’s all over, and credit card balances that are becoming unpaid — 30+ days past due — have been growing all year. In the third quarter, they reached 5.2% of total balances, which is in the same range as during the pre-pandemic lows of early 2016.

“Other” consumer loans, such as personal loans, that are becoming delinquent reached 5.8% of total “other” balances and remain well below pre-pandemic lows:

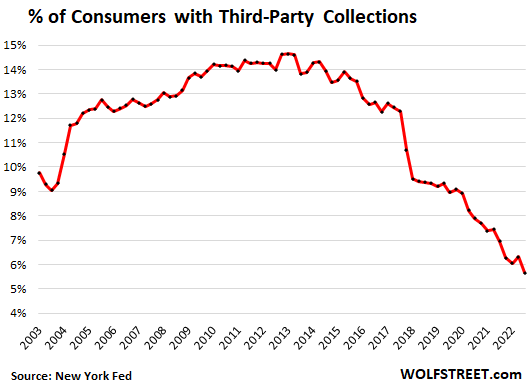

Third-party collections fell to new all-time lows.

The percentage of consumers with third-party collections fell to 5.7%, the lowest on record, and down from 14.6% of all consumers following the unemployment crisis of the Great Recession.

Do you like to read WOLF STREET and want to support it? You can donate. I greatly appreciate it. Click on the mug of beer and iced tea to find out how:

Would you like to be notified by e-mail when WOLF STREET publishes a new article? Register here.

![]()

Image source: Getty Images We’ve all come across an unexpected expense from time to time. Key points 60% of Americans couldn’t cover a $400 emergency expense without going into debt. If you need cash fast and your bank offers payday advances, it might be worth looking into. A personal loan has other advantages, however, such […]]]>

Image source: Getty Images We’ve all come across an unexpected expense from time to time. Key points 60% of Americans couldn’t cover a $400 emergency expense without going into debt. If you need cash fast and your bank offers payday advances, it might be worth looking into. A personal loan has other advantages, however, such […]]]>Image source: Getty Images

We’ve all come across an unexpected expense from time to time.

Key points

- 60% of Americans couldn’t cover a $400 emergency expense without going into debt.

- If you need cash fast and your bank offers payday advances, it might be worth looking into.

- A personal loan has other advantages, however, such as a higher borrowing limit and a lower interest rate.

Many of us have been there. You had a car accident, and now you have to pay the mechanic to fix it. This unexpected expense will cost you a few hundred dollars and, like 60% of Americans, you won’t be able to cover it with your savings. Plus, you only have money for the bare necessities left in your checking account, and your next payday is days away. What should you do?

You have a few options in this situation. Read on to learn more about bank payday advances versus personal loans, and how to decide which is right for you.

What is a salary advance?

A payday advance loan from a bank or credit union is called a small amount loan. These are loans of an amount generally between $100 and $1,000, granted by a bank to account holders. The intention is to give consumers an alternative to predatory payday loans (see below) when they are in a financial bind. If your bank offers them, you’ll get the money you need quickly and pay it back from your next paycheck via direct deposit, or over a period of weeks or months. You will have to pay a fee (either a fixed dollar amount or a small percentage of what you borrow) and interest for the service.

Discover: These personal loans are the best for debt consolidation

More: Prequalify for a personal loan without affecting your credit score

You may soon hear more about payday advances; a Bloomberg Law report in early October 2022 noted that federal regulators want banks to be able to offer them, but banks need more guidance from regulatory agencies moving forward. Personal loans, on the other hand, are already reliably available for your emergency borrowing needs.

What is a personal loan?

A personal loan is a fairly easy way to borrow a lump sum of money. They usually come with lower interest rates than many other quick cash solutions, like credit cards or payday loans (and certainly lower than payday loans). However, if your credit isn’t in top shape, you may not qualify for the best personal loan rates available.

Personal loans are generally in the amount of $1,000 to $100,000, and can often be funded fairly quickly after your application is approved. In some cases, you can get the money the same day or the next day. Is there another way to borrow money quickly? Yes, but you probably want to stay away.

Try to avoid payday loans

Although it may seem counterintuitive (after all, there’s “payday” in the name), it’s a good idea to avoid payday loans. And depending on where you live, they may be illegal in your area; they have been banned in 13 states and the District of Columbia. Payday loans are small, short-term loans of $500 or less, usually with a very high interest rate.

As of 2022, typical payday loan rates range from 28% to 1,950%. These loans often lead consumers into a cycle of debt from which they cannot easily escape. Can’t repay your loan on your next payday? That’s fine, the lender will turn it into a new payday loan for you! How nice of them. Your best choice is probably a payday loan or a personal loan.

How do you choose?

There are a few things to consider when choosing between a payday advance and a personal loan.

How much money do you need?

A payday advance loan, if you can get one from your bank or credit union, is probably best for borrowing smaller amounts. If your auto repair bill is $350, but the smallest personal loan amount you can take out is $1,000, that’s not ideal. If your surprise expense is larger, you’ll likely get a better interest rate with a personal loan (plus, payday loans from your bank may be capped at $500).

How fast do you need it?

If you can wait a few days and have good credit, you may be better off with a personal loan – again, because of interest rates. That said, if your bank offers payday advance loans, they might approve you fairly quickly if you’re an existing customer in good standing. It has already registered you and can access your finances in the form of your bank account(s). Plus, your bank can easily send the money you borrow directly to your account.

How long do you need to pay it back?

This is where a personal loan probably has the advantage. You will have more time to repay a personal loan (months to years) than a payday loan (weeks to months). But again, a lot depends on the amount of money you need to borrow.

Payday advance loans and personal loans have their place, and if you ever get into trouble and need to borrow a relatively small amount of money, both are worth considering. However, it is definitely in your best interest to avoid payday loans.

The Ascent’s Best Personal Loans for 2022

Our team of independent experts have pored over the fine print to find the select personal loans that offer competitive rates and low fees. Start by reviewing The Ascent’s best personal loans for 2022.

NEW YORK, November 10, 2022 /PRNewswire/ — NAF is thrilled to announce a new partnership with Next Gen Personal Finance (NGPF) that will increase access to personal finance education for tens of thousands of students in underinvested communities around the world. nationwide who attend NAF Academies of Finance – small, focused learning communities within existing […]]]>

NEW YORK, November 10, 2022 /PRNewswire/ — NAF is thrilled to announce a new partnership with Next Gen Personal Finance (NGPF) that will increase access to personal finance education for tens of thousands of students in underinvested communities around the world. nationwide who attend NAF Academies of Finance – small, focused learning communities within existing […]]]>NEW YORK, November 10, 2022 /PRNewswire/ — NAF is thrilled to announce a new partnership with Next Gen Personal Finance (NGPF) that will increase access to personal finance education for tens of thousands of students in underinvested communities around the world. nationwide who attend NAF Academies of Finance – small, focused learning communities within existing public high schools.

This partnership supports NAF’s work to address the economic and social disparities that have marginalized too many students in this country with NGPF’s open-source, high-quality, up-to-date personal finance programs and free professional development for students. teachers.

By using NGPF materials and training as an approved curriculum, NAF Academy of Finance teachers can spend more time teaching and building relationships with their students and less time writing ongoing updates. of the program to stay ahead of the ever-changing field of finance.

“We are thrilled to embark on this new partnership with NGPF. A big part of being Future Ready is financial literacy and access to personal finance education is an investment that will pay off for a lifetime,” said CEO of ANF, Lisa Dughi. “NAF students and educators have much to gain from these offerings and will develop many important skills for their next steps in high school and beyond.”

NAF personal finance faculty will use the NGPF’s personal finance and financial algebra semester course syllabi, which are aligned with national standards. Additionally, they will participate in NGPF’s Professional Development (PD) opportunities, which include virtual PD, on-demand modules, and intensive 10-hour certification courses on specific financial topics.

“We welcome the opportunity to share our curriculum and professional development opportunities with NAF Finance Academies and their networks,” said NGPF Co-Founder, Tim Ranzetta. “Personal finance education aligns so well with NAF’s commitment to preparing students for the future.”

To research shows that having a background in personal finance has beneficial effects, including improved credit scores and student loan decisions, and reduced use of payday loans.

Eighty-eight percent of parents want schools to teach personal finance, but only 24% currently do. In communities serving a high percentage of black and Hispanic students and those serving disadvantaged students, access to financial education is only 5%.

For the 2021-2022 academic year, more than 30,000 students participated in 180 NAF Finance Academies across the country. Among these students, 85% were women and/or ethnic minorities. Ninety-eight percent of seniors in NAF academies have graduated, with 87% planning to go on to college. Additionally, NAF Academies focus on other growing industries, including hospitality and tourism, information technology, engineering, and health sciences.

About NAF:

NAF is a national, nonprofit organization that transforms the high school experience to prepare students for college, career, and future success. NAF’s instructional design is uniquely comprehensive in its approach to skills development, enabling students from all backgrounds to participate in a meaningful education and empowering businesses to shape America’s future workforce by transforming the working environment. learning to integrate STEM-infused and career-relevant curricula and work. – Internship-based learning experiences, including.

NAF has evolved from a NAF Academy of Finance to New York City to hundreds of academies across the country focused on growing industries including finance, hospitality and tourism, information technology, engineering, and health sciences; and support curricula that are aligned with the National Career Clusters Framework.

In the 2021-22 school year, more than 120,000 students attended 618 NAF academies in 35 states, plus DC, Porto Rico, and the US Virgin Islands. In 2021, NAF Academies reported that 99% of seniors graduated and 87% of graduates planned to go to college. For more information, please visit: http://naf.org/.

About Next Generation Personal Finance:

Next Generation Personal Finance (NGPF) is a non-profit organization committed to ensuring that all high school students complete a personal finance course before graduating. The NGPF has become the “one-stop-shop” for over 70,000 educators looking for an engaging, high-quality personal finance program to equip students with the skills they need to thrive in the future. NGPF invests in teacher professional development with virtual continuing education workshops, 10 certification courses, and over 40 asynchronous on-demand modules. NGPF has been recognized by Common Sense Education as “the best website for teachers to find lesson plans” and “the best business and financial games”.

Media Contacts:

Courtney Savoydeputy director, communications, NAF, [email protected]

Hannah RaelMarketing Communications Manager, Next Gen Personal Finance, [email protected]

SOURCE Next Generation Personal Finance

Body of the review The fourth annual Halloween pitch competition, hosted by the New Venture Accelerator and the Harbert College of Business, saw 19 teams compete for $5,000 in seed funding, in front of a panel of professional industry judges at the interior of the Broadway Event Space and Theatre. When the scores were tallied, […]]]>

Body of the review The fourth annual Halloween pitch competition, hosted by the New Venture Accelerator and the Harbert College of Business, saw 19 teams compete for $5,000 in seed funding, in front of a panel of professional industry judges at the interior of the Broadway Event Space and Theatre. When the scores were tallied, […]]]>Body of the review

The fourth annual Halloween pitch competition, hosted by the New Venture Accelerator and the Harbert College of Business, saw 19 teams compete for $5,000 in seed funding, in front of a panel of professional industry judges at the interior of the Broadway Event Space and Theatre.

When the scores were tallied, OMNIS came out on top and received $2,000 from the prize pool. OMNIS is a participatory social platform where individuals borrow money through short-term community and peer-to-peer microloans, and where others can borrow money to meet their immediate needs.

Zakariya Veasy, a senior software engineering specialist, founded OMNIS to solve the problem of people with limited credit histories being marginalized by traditional banks and exploited by predatory payday loan companies. “Far too often, the underbanked and unbanked are forced to turn to high-interest payday loans to stay afloat at 400% interest on average,” Veasy said. “The value proposition for OMNIS users is that it builds credit for underserved and neglected demographics. With OMNIS, users build community financial literacy and close generational wealth and credit gaps at across the country.

Other teams that have received funding include:

-

Rodopto, founded by Scott Rowe, uses drones to plant crops that can be converted into renewable diesel fuel and received $1,000.

-

Stretch & Go, founded by Josh Green and Tristin Pettus, is a device providing the critical method for stretching the hamstrings awarded $500

-

BAE, founded by William Murphy and Avery Arasin, is an app that allows students to connect with other students within their own college ecosystem awarded $500

-

AbGlo, founded by Marianne Madsen, Holli Michaels and Courtney Montague, is a fitness device that provides visual feedback to correct lower back posture received the $1,000 Special Category Award provided by the Thomas Walter Center for Technology Management.

The Halloween Business Idea Pitch Contest discovers and rewards early-stage business products, services, or concepts emerging from Auburn University students. Last year’s winner, Room2Room Movers, founded by recent Harbert graduate Brooks Fuller, is currently enjoying significant market success.

Special recognition and appreciation goes to the judges who supported this year’s competition:

-

Sherina Hill, business coach for entrepreneurs

-

Tim Denison, President, GDI LLC

-

Ebony Ruffin, Ruffin Consulting Services

-

Larkin Jones, Alabama Small Business Development Center

-

Ralph Runge, RSquare Consulting, Inc.

-

Jason Wilson, Back Forty Beer

-

Ken Evola, PwC Managing Director, PwC

Comments that competing teams share each year are that, while the prize money is important, ideas and offers of support from alumni, which will help them in their longer-term business planning efforts, are a long way off. the most valuable elements of the experience. It proves once again that the people of Auburn always come back and always give back.

Congratulations to all the teams that participated in the Halloween 2022 pitch contest: Atlas Esports – AbGlo – BAE – Balance Buddy – Bridal Jeans – Drop Out Flags – Flavivirus Resource Center – Gym Rat U – HyperTransport – Kaopetronite – LoLo Baking – Menu Match – OMNIS – Plainsman Financial Consulting – Rodopto – Seat Key – Stretch & Go – Tennis Taps – Your future is today.

NEXT UP: Tiger Cage where startups will compete for $50,000 in seed capital!

Applications to participate in Tiger Cage must be submitted by November 16, with the competition starting on January 27.

To register for Tiger Cage, click here or contact Lou Bifano, Director of the New Venture Accelerator at [email protected] for more information.

Mobile banking is booming. Online payment services are all the rage. These are two of the findings of the Federal Deposit Insurance Corp’s 2021 National Survey. on unbanked and underbanked households, a biennial survey investigation which measures the means and degrees to which Americans access safe and affordable banking services. The agency partnered with the […]]]>

Mobile banking is booming. Online payment services are all the rage. These are two of the findings of the Federal Deposit Insurance Corp’s 2021 National Survey. on unbanked and underbanked households, a biennial survey investigation which measures the means and degrees to which Americans access safe and affordable banking services. The agency partnered with the […]]]>Mobile banking is booming. Online payment services are all the rage.

These are two of the findings of the Federal Deposit Insurance Corp’s 2021 National Survey. on unbanked and underbanked households, a biennial survey investigation which measures the means and degrees to which Americans access safe and affordable banking services. The agency partnered with the US Census Bureau to collect responses from more than 30,000 households in the United States in June 2021.

This year’s survey had a number of takeaways with implications for banking technology, including the prevalence of mobile banking as the primary form of account access, usage patterns of online payment services and technologies that have potentially helped more people obtain banking services or find alternatives. to predatory services. Even though the national unbanked rate has fallen, there are persistent problems with access to banking services among minorities – an issue that has technological implications that are not discussed in detail in the report.

“We’ve had nearly a decade of large-scale digitization of financial services and mass adoption of smartphones,” said Sarah Morgenstern, venture capital partner at Flourish, a venture capital firm that invests in startups. focused on financial health. “This has helped reduce costs and increase access to financial products at fair prices, especially for low- and middle-income consumers.”

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/tronc/KNFAWPLRUNDAFEHTKBXK6GVN4M.jpg) Four years after becoming Lake County treasurer in a 2018 blue wave election, Mundelein Democrat Holly Kim faces a challenge from Republican Paula McGuire of Green Oaks. Kim touts nearly $10 million in investment income earned in 2020, up from $2 million four years ago, the launch of online billing to reduce printing and postage […]]]>

Four years after becoming Lake County treasurer in a 2018 blue wave election, Mundelein Democrat Holly Kim faces a challenge from Republican Paula McGuire of Green Oaks. Kim touts nearly $10 million in investment income earned in 2020, up from $2 million four years ago, the launch of online billing to reduce printing and postage […]]]>Four years after becoming Lake County treasurer in a 2018 blue wave election, Mundelein Democrat Holly Kim faces a challenge from Republican Paula McGuire of Green Oaks.

Kim touts nearly $10 million in investment income earned in 2020, up from $2 million four years ago, the launch of online billing to reduce printing and postage costs and the launch of a 24-hour support system among its achievements.

She also said she had raised the profile of the office from a time when “no one really knew anything about the Treasurer’s Office”, despite a host of challenges presented by the COVID-19 pandemic.

McGuire, a longtime accountant for PwC, says things aren’t going so well and she can usher in changes to better serve Lake County residents.

“I think there’s a fine line in being a PR office and having some sort of fiduciary professionalism in place as well,” McGuire said. “I think the main focus would be to make sure that community assets are properly protected and then you would make sure that individuals in the community actually have access to all the information that they are looking for and maybe you would report, of course on a quarterly basis, what is going on in this office.

Kim took the job with a vision to play a bigger role than just being an office that “just collects the money” from property tax payments and manages a portfolio worth a few hundred million dollars. dollars in county assets.

“It’s true, this office is just collecting the money,” Kim said. “But honestly to God, with the way we invested and returned money, it all helped the county keep its levy flat for three straight years because we got all those extra millions of dollars. So I guess we can help in different ways.

Kim said the increase in investment income was partly due to investments made in ways that his predecessor, David Stolman, “didn’t realize” were available after updates to state laws governing the management of county investments, including the seizure of corporate and municipal bonds. markets.

She added that this raise helps the treasurer’s office “give back millions” so the Lake County Board can then “do things like road projects or flood (mitigation).”

McGuire said she wondered if the wins shared by Kim might be too good to be true.

“If I asked (Kim) specifics about it and how it happened, I’m not sure she could answer that question,” McGuire said. “I found that to be a bit, how do you say that…impossible. If you’re investing according to state regulations and looking at the rates of return over those years, and I don’t want to answer to her question in her place but in my opinion the only way to do that is if you have a huge base influx I kind of tried to press her on that in another situation and she didn’t haven’t really been able to answer the question.

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/tronc/WWBAAVS22ZCP7GFSRON755VWNU.jpg)

McGuire said that if she were to win the job, she would want to ensure that investments are made in clearly permitted areas as defined in state regulations, which she said, “there is a question whether or not this has actually happened in the past here for the past four years.

“Because I’m not a politician, one of the things most people say when dealing with the treasurer’s office is that they want to be more transparent and more specific,” McGuire said.

She said that in order for residents to “get the details” on the desk, “you need the FOIA.”

Kim said she has made other improvements to benefit taxpayers, including reducing eCheck fees to free for online and phone payments, as well as joining the Illinois BankOn Commission, in the part of a mission to get people to avoid taking out payday loans.

“We work with the state; it’s really a move in that we’re moving people away from payday loans and starting a relationship with a bank or credit union instead,” Kim said. “There are a lot of things I’ve been involved in that this office has done to help people.”

McGuire said her “stronghold is numbers” and that she has the financial sense to “act proactively instead of worrying about acting reactively”. A Lake County resident for more than 25 years, McGuire said, she has experience in the insurance industry, banking industry and financial investment services.

She said now was the right time to run for public office since her kids are grown and she’s not one to sit around and complain about things she’d like to see changed, rather than d act to implement them itself.

“With the political climate as it has been for the past five years or so, I don’t think anyone can really sit down and complain about something unless they’re trying to do something,” McGuire said. .

Kim explained that a decision during the pandemic to allow residents to pay their property taxes in four installments shows her ability to adapt and thrive in the role under difficult circumstances.

She said 2022 was the first “normal collection year” during her tenure after figuring out how to handle new software launched by her predecessor, which she said had many “development issues”. Allowing four payments was impractical, Kim said, “but it was the right thing to do.”

“What it did then in the third year that I was here was that we were running two fiscal years, so it was hard for our accounting to catch up,” she said. “There were certain things like the tax sale that we had to pay twice in a year.”

Kim said she’s also taken an active role in advocating for legislative changes that help county residents, including one that ensured more than 5,000 mobile home owners in Lake County would have capped late fees. $100 or 50% of their initial tax bill, as applicable. is lower.

She previously said there were instances in Lake County where customers were unable to pay their property taxes due to accrued late penalties, which she called a policy holdover from politicians who, according to she wanted to “keep the poor in poverty”.

McGuire pointed to a mistake made earlier this year when many residents mistakenly had both installments of their property taxes withdrawn from their bank accounts, instead of the first payment as expected, as evidence that a change is needed. locally.

Kim explained in a June Facebook post that the double charge happened due to “human error.”

McGuire, as well as some people who commented on Kim’s post, criticized the error for possibly causing bank accounts to be overdrawn, resulting in overdraft fees, and even the disruption of other scheduled payments.

“My question is, how do you split this process of two payments into four payments, but not test it enough to make sure it’s not going to double?” McGuire said. “I don’t understand how this could have happened.”

Image source: Getty Images When you’re in a bind and need cash fast, it’s important to know what your options are. There are different types of loans that you can get relatively quickly, depending on your needs. Before getting a personal loan, it’s important to understand the different types of personal loans and find the […]]]>

Image source: Getty Images When you’re in a bind and need cash fast, it’s important to know what your options are. There are different types of loans that you can get relatively quickly, depending on your needs. Before getting a personal loan, it’s important to understand the different types of personal loans and find the […]]]>Image source: Getty Images

When you’re in a bind and need cash fast, it’s important to know what your options are. There are different types of loans that you can get relatively quickly, depending on your needs. Before getting a personal loan, it’s important to understand the different types of personal loans and find the right one for you. Here are four of the most common.

1. Credit cards

If you have good credit, you may be able to get a cash advance on your credit card. This is usually a quick and easy process, but it will come with high interest rates. So if you are able to repay the loan quickly, this could be a good option. Cash advances can be very useful in an emergency situation when you need money immediately.

Discover: These personal loans are the best for debt consolidation

More: Prequalify for a personal loan without affecting your credit score

Another advantage of using a credit card for a cash advance is that you may already have money available on your line of credit that you can use. This can be useful if you don’t want to take out a new loan or use other assets as collateral. However, using a credit card for a cash advance also has some drawbacks. First, as mentioned earlier, interest rates on cash advances are usually very high. This means that if you don’t repay the loan quickly, you could end up paying a lot of interest. Also, most credit cards have limits on how much you can borrow as a loan. So if you need a large sum of money, this might not be the best option.

2. Payday Loans

Payday loans are one of the fastest ways to get cash, but they come with high interest rates and fees. They’re usually only for small amounts of money, so if you need a lot of cash quickly, they’re probably not the best option. However, if you just need a little extra money to last you until your next paycheck, a payday loan might work. Payday loans are not ideal, however. These are short-term, high-interest loans, usually due by your next payday in a single amount. Currently, 37 states regulate payday loans due to their high costs.

Payday loans are usually for $500 or less and are due on your next payday. Depending on state laws, people can get payday loans online or through a storefront lender. A typical two-week payday loan can have annual percentage rates (APR) as high as 400%. By comparison, credit card APRs can range from 12% to 30%. Payday loans should be considered an option of last resort.

3. Pawnbroker

Pawnbrokers are short-term loans secured by an object of value that people bring to a pawnbroker. As they are backed by the value of the object, they are cheaper than payday loans but are more expensive than a conventional loan. Pawnbrokers are regulated by the government. This type of loan is ideal for people who need cash quickly without a credit check.

Loan terms vary by pawnbroker. People can use valuables, such as jewelry or electronics, to get a loan based on the value of the item. No credit check is required. Those who may not qualify for a traditional loan can consider a pawnbroker. Once the loan amount is paid off, you will receive your items. If you don’t pay it back, the pawnbroker can seize the secured items.

4. Securities Lending

Title loans are another quick way to get cash. These are short-term secured personal loans secured by your car. Financial institutions put a lien on your car. If you are unable to repay the loan, they can seize your car, as it is used as collateral. Title loans generally do not consider your credit and can be approved quickly. However, a title loan is very expensive, with an APR of around 300%.

These are four of the most common types of loans that you can get relatively quickly. Consider which one best suits your needs and compare interest rates and fees before you apply. Understanding how these personal loans work can help you make a smarter decision.

The Ascent’s Best Personal Loans for 2022

Our team of independent experts have pored over the fine print to find the select personal loans that offer competitive rates and low fees. Start by reviewing The Ascent’s best personal loans for 2022.

We are firm believers in the Golden Rule, which is why editorial opinions are our own and have not been previously reviewed, approved or endorsed by the advertisers included. The Ascent does not cover all offers on the market. The editorial content of The Ascent is separate from the editorial content of The Motley Fool and is created by a different team of analysts. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

On October 20, the Federal Trade Commission (FTC) Posted an advance notice of proposed rulemaking, seeking public comment on the harms resulting from what it describes as “undesirable fees”, that’s to say, allegedly unnecessary, unavoidable or unexpected charges that inflate costs while adding little value. The term also encompasses “hidden charges”, which are charges for […]]]>

On October 20, the Federal Trade Commission (FTC) Posted an advance notice of proposed rulemaking, seeking public comment on the harms resulting from what it describes as “undesirable fees”, that’s to say, allegedly unnecessary, unavoidable or unexpected charges that inflate costs while adding little value. The term also encompasses “hidden charges”, which are charges for […]]]>On October 20, the Federal Trade Commission (FTC) Posted an advance notice of proposed rulemaking, seeking public comment on the harms resulting from what it describes as “undesirable fees”, that’s to say, allegedly unnecessary, unavoidable or unexpected charges that inflate costs while adding little value. The term also encompasses “hidden charges”, which are charges for goods or services that are misleading or unfair, including because they are disclosed only at the last stage of the consumer’s purchase process or not everything. Although the FTC has been active in bringing enforcement action against alleged “junk fees,” it generally lacks the authority to seek sanctions against first-time offenders or the ability to obtain financial compensation for consumers in cases where “junk fees” violate the FTC. prohibition of unfair or deceptive practices. This new rule would change that.

According to the FTC, these so-called “junk fees” are prevalent in a variety of industries: “Junk fees manifest themselves in markets ranging from auto financing to international calling cards and payday loans. Examples of fees the FTC is questioning include “mobile cramming” fees, connection and maintenance fees on prepaid phone cards, account fees, fees that decrease the amount a borrower receives from loan, miscellaneous fuel card charges, car dealership fees, undisclosed fees for funeral services, hotel “resort” fees, hidden fees for academic publications, poorly disclosed auxiliary insurance and membership programs.

According to the FTC, the fees it plans to regulate fall into the following categories:

- Unnecessary charges for worthless, free or counterfeit products or services.

- Consumers may be subject to fees for products or services that cost businesses nothing, are available free of charge, or should be included in the purchase price.

- Unavoidable charges imposed on captive consumers.

- Consumers may be forced to pay unwanted charges because they have no way of avoiding or opting out of them, either because they are dealing with a monopolistic company or because they have already invested money in the product or service and can’t easily walk away.

- Surprise fees that secretly drive up the purchase price.

- According to the FTC, this happens when companies unexpectedly prey on undisclosed fees, hide fees in the fine print, add fees at the end of a purchase process, or use digital dark models or other deceptions to perceive them.

The FTC invites comment on, among other things, the prevalence of each of the above practices and the costs and benefits of a rule that would require the initial inclusion of all mandatory charges whenever consumers are offered a price for a good or service. Once the notice is published in the Federal Registerconsumers can submit their comments electronically.

This proposed rule isn’t the only new rule the FTC is considering attacking fees. As we discussed here, in June 2022, the FTC issued a proposed motor vehicle dealer business regulation rule. The proposed rule would create a host of new compliance challenges for motor vehicle dealers, including a new national standard for advertising prices, disclosure triggers for payments, additional paperwork for selling add-on products, prohibition of “no benefit” additions on products and additional record keeping requirements. The deadline for comments expired on September 12.

The FTC and other regulators have also challenged the charges through enforcement action, and this notice follows the FTC’s announcement of charges against a car dealership for discriminating against certain groups of car buyers in the way he imposed additional charges in the automobile. vehicle sales. We are discussing this settlement here.

FTC Chair Lina Khan explained the reasoning for the proposed new rule in her statement“These types of additional or redundant charges can mislead consumers or prevent them from knowing the true cost of a purchase until they have already invested significant time and energy.” Chairman Khan also claimed that the “unwanted fees” also had negative ramifications for other business owners. “These fees don’t just hurt consumers, they can also force honest businesses to compete on an unfair playing field. A company selling a widget for $25 could lose sales to a company selling a comparable widget for $20, plus a six-dollar widget certification fee added at the end.

Troutman Pepper will continue to monitor important developments involving the FTC and the proposed rules, and we will provide further updates as they become available.

Amada Senior Care employees now have access to financial health with ZayZoon PHOENIX, Oct. 18, 2022 (GLOBE NEWSWIRE) — ZayZoon, the provider of access to earned wages for small and medium-sized businesses, today announced a partnership with Amada Senior Care, a company focused on enriching lives by providing nurturing and compassionate home care to ensure […]]]>

Amada Senior Care employees now have access to financial health with ZayZoon PHOENIX, Oct. 18, 2022 (GLOBE NEWSWIRE) — ZayZoon, the provider of access to earned wages for small and medium-sized businesses, today announced a partnership with Amada Senior Care, a company focused on enriching lives by providing nurturing and compassionate home care to ensure […]]]>Amada Senior Care employees now have access to financial health with ZayZoon

PHOENIX, Oct. 18, 2022 (GLOBE NEWSWIRE) — ZayZoon, the provider of access to earned wages for small and medium-sized businesses, today announced a partnership with Amada Senior Care, a company focused on enriching lives by providing nurturing and compassionate home care to ensure their staff have the financial flexibility they deserve. With more than 120 locations, thousands of Amada employees provide home care and assisted living services to seniors in 37 states.

Thirty-one Amada locations have already activated ZayZoon and more than 750 employees have signed up for instant access to their pay as they earn it, without having to wait for their regular paycheck. In addition to ZayZoon’s on-demand salaries, Amada staff also have access to free financial education and retailer rewards, which can save customers hundreds of dollars on everyday purchases.

“We wanted to provide our employees with a benefit that is accessible to all and desired by most. ZayZoon is a fully standalone solution that has proven impact in improving retention, which made it easy to decide to offer this benefit to our staff,” said Rick Basch, COO of Amada Senior Care Franchise.

ZayZoon makes its products available to all employees, whether hourly or salaried. In a world where there are many ticked benefits available that don’t offer much benefit, it’s common for a company to have over 30% of its workforce using ZayZoon on a regular basis. In a survey, 89% of customers said ZayZoon helped them reduce financial stress.

About Amada Senior Care

Amada Senior Care, formerly Amada Home Care, was founded in 2007 by college friends Tafa Jefferson and Chad Fotheringham. Today, Amada Senior Care has more than 120 locations across the United States and is committed to enriching lives by providing caring, compassionate home care for seniors and guiding families through the many housing options. for seniors available for assisted living. Healthcare professionals and families turn to Amada to help them navigate the complexities of the senior care system.

About ZayZoon

ZayZoon is on a mission to improve employee health through the use of responsible financial products. Unfortunately, millions of Americans rely on predatory products like payday loans and overdraft fees to bridge the paycheck gap created by predetermined payroll cycles. With their products including on-demand salaries, financial education, and retail rewards, ZayZoon helps break this cycle. ZayZoon’s on-demand access to salaries helps reduce financial stress and improve job satisfaction and productivity.

Contact information:

Shannon Dougall

Senior Vice President, Marketing

[email protected]

This content was posted through the press release distribution service on Newswire.com.